Insurance

IP Bulletin

An Information Bulletin on

Intellectual Property activities in the insurance

industry

A Publication of -

Tom Bakos Consulting, Inc. and Markets, Patents and Alliances,

LLC |

June 15, 2006

VOL: 2006.3

|

Publisher

Contacts

Introduction

In this issue’s feature article, What’s In a Name: Choosing an Effective Trademark, our guest author, Leora Herrmann, Esq., takes a look at trademarks, the other activity of the United States Patent and Trademark Office (USPTO). She notes that, Shakespeare notwithstanding, there is something in a name.

In our Patent Q/A section we talk about how to use a Petition to Make Special to accelerate the examination of your patent application so that you can get a business method patent to issue in as little as 2 years instead of the normal 5 or more years.

We also discuss the basics of how insurance works in a new Basic Ed. feature: Insurance is a Process of Processes. We do this in order to bring to our readers who may not be too deeply involved in the business of insurance some basic understanding of just what is going on that may be inspiring the innovative spirit. We expect to follow this up in future issues with more explanation and would welcome reader comments on subject areas we ought to consider first.

The Statistics section updates the current status of issued US patents and published patent applications in the insurance class (i.e. 705/004). We also provide a link to the Insurance IP Supplement with more detailed information on recently published patent applications and issued patents.

Our mission is to provide our readers with useful information on how intellectual property in the insurance industry can be and is being protected – primarily through the use of patents. We will provide a forum in which insurance IP leaders can share the challenges they have faced and the solutions they have developed for incorporating patents into their corporate culture.

Please use the FEEDBACK link to provide us with your comments or suggestions. Use QUESTIONS for any inquiries. To be added to the Insurance IP Bulletin e-mail distribution list, click on ADD ME. To be removed from our distribution list, click on REMOVE ME.

Thanks,

Tom Bakos & Mark Nowotarski

Feature

Article

What’s In a Name: Choosing An Effective Trademark

By:

Leora Herrmann, Esq., Partner, Kluger, Peretz, Kaplan & Berlin, lherrmann@kpkb.com http://www.kpkb.com/professionals-28.html"What’s in a name? That which we call a rose by any other name would smell as sweet." So spoke the heroine in Shakespeare’s Romeo and Juliet. Juliet’s sentiment rang true in the

Bard’s tale of star-crossed lovers. But, when it comes to business, she couldn’t

have been farther from the mark.

In insurance, as in any other industry, names are the key to effective marketing. They differentiate one company or product from all others, enable customer loyalty and foster goodwill.

The names (and logos) companies use for their goods and services are protected by the law of trademarks, a branch of intellectual property law. Trademark law gives the owner of a valid trademark a monopoly that allows it to stop others from adopting any confusingly similar mark for related goods or services.

A trademark monopoly is best established by registering one’s trademark with the United States Patent and Trademark Office (USPTO). A federal trademark application can be filed as soon as a company has a bona fide intent to use the mark. This gives the applicant nationwide priority over others who later adopt the same or a similar mark for related goods or services.

But not all names qualify for trademark protection. The key is to choose a protectible name that does not infringe on others’ established trademark rights. As Shakespeare would say, "There’s the rub."

First, in choosing a trademark, avoid generic terms. The generic names for goods or services belong to the public at large and cannot be monopolized by a single company. Just as no one can claim "automobile" as a trademark for cars, any word that is the generic name for an insurance product is off limits as a trademark.

Descriptive terms are a step in the right direction, but still difficult to protect. In 2005, Allianz Life Insurance Company of North America’s application to register WEALTHCARE as a trademark for healthcare insurance, life insurance and annuities was rejected by the USPTO because "the term WEALTHCARE is merely descriptive of a function or purpose of Applicant’s insurance services, that is, to care for or manage the insured’s wealth."

Descriptive terms like WEALTHCARE are not given trademark status unless and until they have been so widely advertised and used that they have acquired "secondary meaning" with the public; that is, the public has learned to recognize them as trademarks despite their descriptiveness. In the case of WEALTHCARE, the USPTO found that Allianz had not shown that "relevant customers of such insurance services have come to view WEALTHCARE as Applicant’s source-identifying mark," rather than a mere description of the insurance that Allianz offered. As a result, trademark protection was denied. To avoid this fate, stay away from descriptive marks.

A better choice for a trademark is a term or phrase that is "suggestive." Suggestive marks evoke an image related to the product or service, but do not describe it. They are protectible without proof of secondary meaning. In a recent federal lawsuit, the court held that CAREFIRST is a suggestive trademark for health insurance and related services because "CareFirst connotes some kind of health-related service or product, although consumers would be unlikely to identify the service or product without actual knowledge of it."

Fanciful and arbitrary terms make the best marks. KODAK – a coined term – is a fanciful mark and APPLE for computers is arbitrary. Marks like these, which do not describe or even suggest the goods and services for which they are used, are the strongest and most easily protectible. They may, however, be less desirable for marketing purposes. A suggestive mark like CAREFIRST connotes reliability, compassion and responsiveness. It’s more difficult for an arbitrary or fanciful mark to evoke such sentiments.

The selection of a protectible term is the first step in choosing a trademark. The second is to determine, with as much confidence as possible, that the mark will not infringe existing third party trademark rights; that is, that the mark is available. This evaluation should be performed by a qualified trademark attorney who will first conduct and commission a trademark search to identify third parties who have registered or are using identical or similar marks. If the mark will be used internationally, foreign trademark searches must also be commissioned and evaluated.

Just because a search reveals that the term is already being used as a trademark does not mean that it is off limits. Trademark availability depends on whether simultaneous use of both marks will create a likelihood of confusion among purchasers. This is determined by weighing such factors as the strength of the prior trademark, the similarity of the marks, the similarity of the parties’ goods and services, the sophistication of the relevant group of consumers, and the extent to which advertising and distribution channels overlap.

Clearly, under the right circumstances, the same word can be used as a mark in different fields without confusing the public. No one mistakenly concludes that Delta Airlines is the source of Delta faucets, or that the Ford Modeling Agency is the source of Ford automobiles.

However, where the parties’ goods and services are more closely related, a likelihood of confusion may arise. Thus, some years ago, Guardian Life Insurance Company succeeded in getting an injunction against an independent insurance agency barring it from using the name Guardian Group-Gerardi Associates as its service mark. (A service mark is nothing more than a trademark that is used to identify the source of services.) Even though the agency’s sales of life, group and business health insurance amounted to only 5.75% of its business, the court concluded that consumers were likely to conclude that the agency was affiliated with Guardian Life and ordered it to stop using "Guardian" in its name.

Choosing a trademark can involve multiple false starts. The obvious "good names" are often already taken. But with creativity, persistence and good legal advice, a trademark that is effective, available and protectible can always be found.

NOTE: More information about trademarks is available at the USPTO Trademark web site:

http://www.uspto.gov/main/trademarks.htm

Patent Q & A

Title: Accelerated Examination

Question: Is there anyway I can speed up the process

for getting a patent?

Disclaimer: The answer below is a discussion of typical practices and is not to be construed as legal advice of any kind. Readers are encouraged to consult with qualified counsel to answer their personal legal questions.

Answer: Yes, It’s called a Petition to Make Special

(PTMS)

Details: "You know", said John Love, "I don’t know

why more inventors don’t use the Petition to Make Special. It would really speed

up the examination of their applications." John was the director of art unit

3600 at the USPTO at the time. Art unit 3600 includes business methods. I was

chatting with him as we were walking down the hall of the patent office about

the problem of unusually long delays in getting business method patents

examined. With the step increase in business method filings after the State

Street Bank decision in 1998, the heightened scrutiny that the patent office was

giving to business method patents and the ongoing challenges of hiring and

training qualified patent examiners in this area, delays in getting an examiner

to look at an application (i.e. issue a first office action) had stretched out

to over four years. John reminded me, however, of an option that all patent

agents and attorneys should know about, the Petition to Make Special. In

essence, anyone can have their application examined early if they submit a

petition that meets certain criteria.

A Petition to Make Special is a formal request submitted to the patent office asking that your patent application be examined ahead of the other pending applications in the same technological art. Normally patent applications in a given technological art are examined in the order that they are filed in. First come, first served. The patent office has realized, however, that some inventions deserve special attention and that patent applications covering these inventions should be examined as quickly as possible. If your invention falls into one of the special categories, you can petition to have it examined early.

Some of these categories are related to the benefits of the invention. If your invention is related to countering terrorism, energy conservation or improvements in environmental quality, for example, it qualifies for special status.

Some of these categories are related to the status of the inventor. If one of the inventors is over the age of 65 or in very poor health, the patent application qualifies for special status.

Some of these categories are related to the commercial status of your invention. If your invention is being actively infringed, or if you can show that an issued patent is required in order for you to start manufacturing your invention, then your patent application may qualify for special status.

There is a final category that almost any invention can qualify for. This is a Petition to Make Special for Accelerated Examination. This is the category that is most relevant to business method inventions, including those in the insurance industry.

A PTMS for Accelerated Examination is granted if the applicant (e.g. the inventor) is willing to perform a substantial amount of the work of examining their own application. The applicant must, for example, have an independent qualified third party perform a prior art search using the same standards that the patent office uses. The applicant must also submit an analysis of the prior art showing why their invention is allowable despite what is taught by the prior art. The costs of the search and analysis are significant and there are some risks involved (be sure to discuss these with your patent agent/attorney), but experience has shown that a PTMS for Accelerated Examination can cut the time to get a patent to issue in the business method area from more than 5 years to less than 2. We’ve seen first office actions issued in as little as 6 months from the filing date of the application and notices of allowable subject matter in just over a year.

Inventors can get relatively fast action on their business method patent applications if they qualify for a Petition to Make Special. First see of your patent application falls into one of the categories reserved for special treatment, such as an anti-terrorist invention, an application where one of the inventors is over the age of 65, or an invention that is actively being infringed. If it doesn’t fall into one of the categories for special treatment, then consider a PTMS for Accelerated Examination. Be sure, however, to discuss the costs and risks with your patent agent/attorney. If your petition is accepted and all goes well in the examination, you can get a business method patent to issue in much less time than would otherwise be expected.

Note: More details on the rules for Petitions to Make Special can be found online at

http://www.uspto.gov/web/offices/pac/mpep/documents/0700_708_02.htm

Basic Ed.

Insurance is a Process of Processes -

Contingent Events

Our mission has been to provide useful information on how innovation in the insurance industry can be protected with patents, principally, but also with trademarks and copyright. The presumption has been that our readers were already fairly familiar with the business of insurance. So, we have focused on providing education and insight into IP protection processes.

In order to understand innovation and invention in the insurance business, it is very helpful to understand insurance. We find that the presumption that our readers are well versed in insurance principles and only need help understanding the IP protection side is not 100% correct. Many have a greater understanding of the patent processes than they do of the insuring processes which can present just as great a difficulty in identifying invention as the other way around. So, we will try to address this void by providing in this Basic Ed. column some basics on insurance. We hope that it will be informative to all of our readers.

The first thing to recognize is that insurance is a process – actually, it is a process of processes. It is this fact that makes inventive insurance processes, or business methods, patentable. As patent savvy people know, there are four categories of patentable subject matter: articles of manufacture, compositions of matter, machines, and processes. Insurance business methods fall primarily into the process category, and, to the extent computers are involved, the machine category.

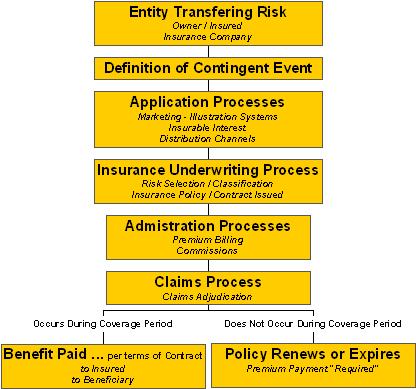

One schematic of the various processes making up the overall insurance process is shown in the chart.

This schematic splits the overall insurance process into eight more elementary processes. Insurance innovators seek solutions, or better solutions, to problems in these elementary processes.

The most essential process is the Definition of Contingent Event process since this process identifies what is being insured and effects in some way all of the others. We are, therefore, going to address what a contingent event is first and its relationship to risk.

Generally, risk means an exposure to loss or damage as a result of the possible occurrence of a contingent event. A contingent event is an event which is uncertain with respect to its occurrence, timing, or severity. Typically, loss or damage is expressed in terms of dollars.

For example, driving exposes you to the risk that you may crash your automobile or be involved in a crash. A crash may or may not happen (occurrence) and its severity can vary - fender bender vs. total destruction. Winning the lottery is also a contingent event (assuming you bought a ticket) with respect to its occurrence. Living exposes you to death at some point in your life. We are not immortal so death is certain – only its timing is usually uncertain. That is, we may live to a ripe old age, die earlier than old age as a result of sickness, or suddenly by accident.

Winning the lottery would be a good thing so, severity, may not be the most appropriate word to use to describe your lottery winnings but the amount of your winnings will depend upon how many others also chose the same winning numbers. Your death is the loss of your life and your life has a value which may be quantified in terms of future earnings lost. A death may also create a financial strain as a result of the inability it causes to satisfy some expected promise of performance. The need to repair or replace your car following a crash quantifies the financial consequences of an automobile accident. Similarly, any property insurance can be quantified in terms of the repair or replacement cost.

Insurable events are a sub-set of contingent events.

Insurable events are contingent events which result in some adverse financial

consequence to someone and have a relatively low probability of occurring.

Insurance is, essentially, a way to manage the financial consequences of risk.

The basic insurance process transfers the financial consequences of risk from one entity to another for a premium. Insurance is evidenced by a legal contract – the insurance policy.

Contingent events that occur with relatively high frequency and for which there is little uncertainty with respect to their occurrence or timing are not insurable because there are better ways to address the financial consequences. Pregnancy, for example, though it has financial consequences, is not really an insurable event because to a certain extent it can be planned and budgeted for. Medical complications resulting from pregnancy, however, are uncertain and can be considered insurable events.

Equity in insurance requires that individuals who

pay a premium for their insurance be grouped or pooled with other individuals

who are exposed to the same risks and have the same or, at least, a similar

expectation of loss associated with the occurrence of the insured contingent

event.

Equity in insurance is a fairness issue but it also has a practical side. The premium charged for insurance is a kind of pooling cost that all members of a risk class agree to pay into the risk class pool in order to receive a larger benefit from the risk class if the insured contingent event happens to them. An individual who feels that they are being charged too much relative to the others in the pool for the risk they are transferring to the pool, will tend to not join. Those who feel their risk is greater than what is being charged to join will join the pool more readily. In order to maintain equity, the insurance company uses a risk selection process called underwriting to select and classify risk in order to determine an appropriate premium to charge for the risk transfer process.

Contingent events that occur very infrequently and that have huge financial consequences may be uninsurable for practical reasons. That is, there is either no entity willing or able to accept through an insurance process such a financial consequence or no one would willing to pay the premium required for an event with such a low frequency – even though its occurrence would be devastating.

Insurance is a process of processes. An early step in the process is defining the contingent event that is being insured against. Contingent events are considered to be insurable if the frequency is relatively low, the financial impact is relatively high (but not too high) and the occurrence is largely outside of the control of the insured. Improvements in the process of defining insurable contingent events is an important area of innovation in the insurance industry, and can lead to patentable inventions.

Statistics

An Update on Current Patent Activity

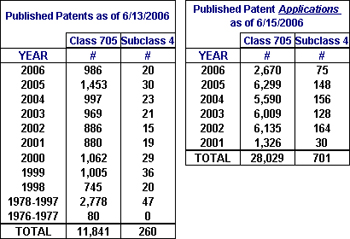

The table below provides the latest statistics in overall class 705 and subclass 4. The data shows issued patents and published patent applications for this class and subclass.

Class 705 is defined as: DATA PROCESSING: FINANCIAL, BUSINESS PRACTICE, MANAGEMENT, OR COST/PRICE DETERMINATION.

Subclass 4 is used to identify claims in class 705 which are related to: Insurance (e.g., computer implemented system or method for writing insurance policy, processing insurance claim, etc.).

Issued Patents

Since our last issue, 9 new patents with claims in class 705/4 have been issued: 4 relate primarily to L&H, 2 relate to P&C insurance in general; and 3 appear to have applications in all lines. Five of these nine newly issued patents have an assignee indicated. The other four are to independent inventors.

Patents are categorized based on their claims. Some of these newly issued patents, therefore, may have only a slight link to insurance based on only one or a small number of the claims therein.

The Resources section provides a link to a detailed list of these newly issued patents.

Published Patent Applications

Thirty eight (38) new patent applications with

claims in class 705/4 have been published since our last issue. They are broken

down by product line or type area as follows:

P&C:

16

Life & Health 20

All:

2

TOTAL: 22

The Resources section provides a link to a detailed list of these newly published patent applications.

Again, a reminder -

Patent applications have been published 18 months after their filing date only since March 15, 2001. Therefore, there are many pending applications that are not yet published. A conservative assumption would be that there are, currently, about 200 new patent applications filed every 18 months in class 705/4.

The published patent applications included in the table above are not reduced when applications are either issued as patents or abandoned. Therefore, the table only gives an indication of the number of patent applications currently pending.

Resources

Recently published U.S. Patents and U.S. Patent Applications with claims in class 705/4.

The following are links to web sites which contain information helpful to understanding intellectual property.

United States Patent and Trademark Office (USPTO)

: Homepage - http://www.uspto.gov

United States Patent and Trademark Office (USPTO)

: Patent Application Information Retrieval - http://portal.uspto.gov/external/portal/pair

Free Patents Online

- http://www.freepatentsonline.com/

World Intellectual Property Organization (WIPO)

- http://www.wipo.org/pct/en

Patent Law and Regulation

- http://www.uspto.gov/web/patents/legis.htm

Here is how to call the USPTO Inventors Assistance Center:

- Dial the USPTO’s main number, 1 (800) 786-9199.

- At the first prompt press 2.

- At the second prompt press 4.

- You will then be connected to an operator.

- Ask to be connected to the Inventors Assistance

Center.

- You will then listen to a prerecorded message before being connected to a person who can help you.

The following links will take you to the authors’ websites

Mark Nowotarski - Patent Agent services

– http://www.marketsandpatents.com/

Tom Bakos, FSA, MAAA - Actuarial services

– http://www.BakosEnterprises.com